What are the biggest challenges you are facing in your business right now? I just posted this question on a small business group that I’m a member of on Alignable.com.

As a partner in a consulting firm, we are putting together updated, post pandemic marketing materials and fine tuning our message. I wanted to get an idea of the biggest problems companies are currently facing. Our economy has been through a lot the past few years. The responses I received were wide ranging and touched upon just about every area of business (with some surprises): delegating, ADHD, growing the business, raising capital, finding employees, raising prices, staying motivated, prioritizing, and closing sales to name several. I thanked all of those who replied and contributed some tidbits of advice. I couldn’t help myself. As a consultant, that’s what I do. One particular response was a business having difficulty getting his salespeople to close at a rate above 10–15%. I replied that he should check his industry’s standard closing rate because maybe 10–15% was within the norm. Many a company I’ve consulted would be thrilled with a 15% closing rate. (The average sales success rate across all industries is 3%.) I also suggested some sales training, because while research has been mixed on the effectiveness of sales training, some studies suggest it can improve ROI considerably. Lastly, I suggested his sales staff read the book, “The Asking Formula,” by John Baker. It really is a wonderful little book for sales and I recommend that everyone read it regardless of what they’re doing. He rather sanctimoniously said that he already has three sales trainers that he feels are the best in the world. One of them made $33 million in commissions in 10 years. And that, someone will not rise to his level reading from a book. Okay, but, what? Obvious first question, Why not use that guy for your sales instead of as a trainer? Maybe he’s retired? So, Why is your sales staff still struggling with the $33 million guy training them? Along with the gold, there’s a lot of questions in “them thar hills.” A Method to Find out What Your Problem Really Is It brought to mind the Startup Founders Group I was a founding member of many years ago. We met once a month to process issues. We started with a dozen or so entrepreneurs and I appreciated it because being a Startup Founder without a partner can be a lonely endeavor. We had a formal approach for processing our issues: Begin with a problem and put it into a question. It should take the form of How Do I (HDI). It can be business or personal, because if you’re having personal problems, it can definitely interfere with your business. After the issue was presented, there was a period of questions which the founder would answer. After that the other members would suggest a different HDI. We found that the problem members thought they were having, wasn’t really the problem. Almost always! Here are some hypothetical HDIs to give you an idea of the concept. 1. HDI increase my runway by raising money in a hurry? Could actually be, HDI cut expenses to decrease my monthly burn rate? 2. HDI deal with my partner who is an alcoholic and passing out in the middle of the day? Could be, HDI buy out my partner? (Ask him when he’s on a bender with pen and contract in hand. Just kidding.) 3. HDI reduce my dependency on one large customer? Try, HDI divert resources and update my marketing plan to attract new, smaller customers? 4. HDI get my spouse to be more supportive of my startup? HDI improve my communication skills so that my spouse understands the startup world. After the HDI is restated and accepted by the processing member of the group, (and they can choose between many suggested HDIs, or even their original HDI), we would enter the period of suggestions. These are ideas of how the member can fix their problem. During this period they need to remain silent and listen. We assign another member to take notes, so the issue processor can just listen. Upon finishing, the member taking notes will email those to the processor and then, the most important part, they make a promise or commitment to action (CTA). Relevant Questions to Ask Back to the sales guy on Alignable.com. The following are the types of questions he should ask himself after the first two obvious questions I mentioned earlier. Keep in mind some of the questions here included what are called, veiled suggestions. When you are processing, just ask questions. But for this article, I’ll include some suggestions along with the questions. 1. Again, what is the industry average closing rate? You didn’t answer that. 2. The $33 million guy might be a great closer, but a lousy teacher. That’s possible. Can he teach others? Perhaps he doesn’t like the task of training others? 3. Are the sales people you’re hiring any good at sales? Start keeping track of your sales data; who is the most successful and what are their methods? 4. If your sales people are underperforming, is there a problem with your product? 5. Ask top level interviewees that are declining to take a sales job with you, why? Maybe you need to offer a higher salary, commission rate or benefits. 6. In addition to training people to sell, are you training them about your products, all the benefits? 7. If appropriate, do you have a good prepared pitch? If not, maybe you need one. If so, maybe it needs to be better. 8. Are you providing your sales staff with good quality, warm leads? If not, maybe you could do that. 9. Is your product a commodity, based simply on price? If so, maybe you need to adjust your pricing. 10. If your product is not a commodity, have you developed reasons why customers should buy from you? Have you distinguished your company through customer service, or some other benefits? 11. Do you have a detailed marketing program to support your sales people? Do you have a marketing strategy at all? I could go on. But after all these questions are answered I think a new HDI suggestion would be along the lines of: How do I help my sales staff to be more successful? Then move on to the suggestions phase, many of which will be self-evident. That is the value of questioning whatever you think your problem is. You can use this process yourself, with your own company, for any issues you are facing. Better yet, get your employees to join in. They might know more than you. They’re on the front lines, after all. Originally published at https://www.datadriveninvestor.com on February 24, 2023. Subscribe to DDIntel Here. Visit our website here: https://www.datadriveninvestor.com

0 Comments

And help their customers along with their own bottom line.  Photo by Author It is always a win-win for financial institutions to reduce loan delinquencies. This has become especially important during the post-pandemic world with a slumping housing market, high inflation, raising interest rates and high levels of consumer debt. During the economic shocks of the last few years, however, we saw an interesting trend in delinquencies.

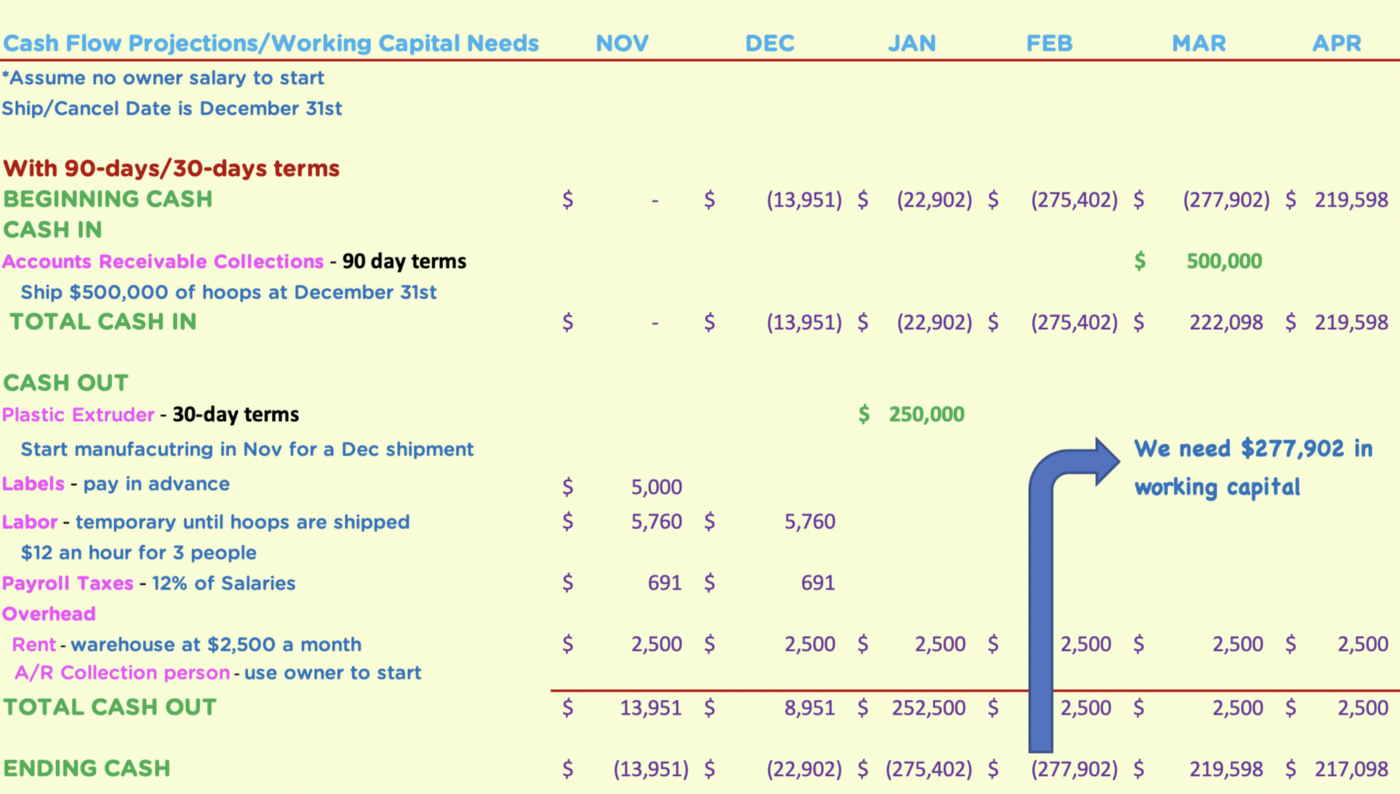

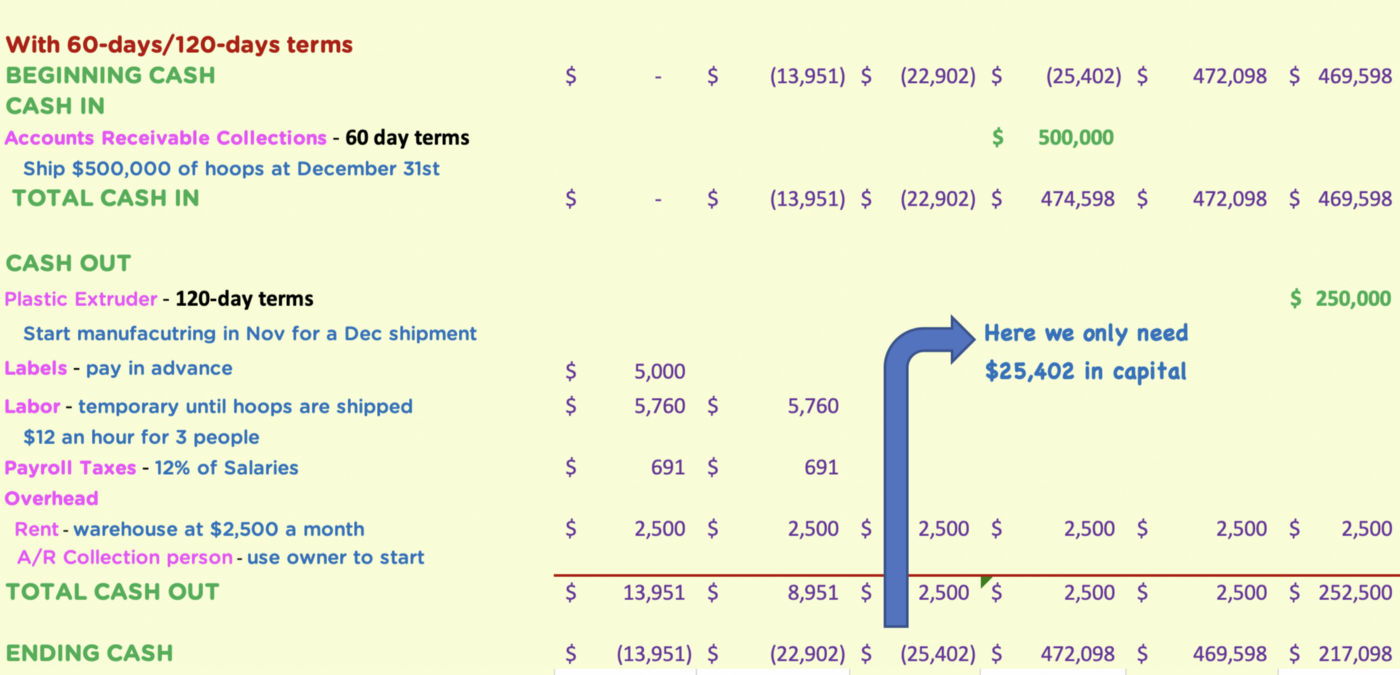

Spanish philosopher George Santayana is credited with the aphorism, “Those who cannot remember the past are condemned to repeat it.” As we navigate our current economic challenges, looking back at our most recent economic downturn, the Great Recession in the late 2000s, might provide some helpful lessons. In early 2009, I attended an economic forum with guest speakers from the banking, real estate, stock brokerage, and economic industries. At that time, there were many real estate properties in foreclosure, but the banks didn’t seem very interested in selling them. My favorite part of the forum is when the banking executive told me why. Banks had such an excess of properties in foreclosure on their books, that to sell them at their market value (about 40% less than book value), and write-off the losses would have rendered the financial institutions insolvent. So they just didn’t sell them. During the pandemic years of 2020 and 2021, the unemployment rate from the Bureau of Labor Statistics showed both the unemployment rate at 6.2 percent, and the number of unemployed persons at 10 million. However, loan delinquencies went down — even with the high unemployment rate and the strong historical association between the unemployment rate and loan defaults. A 2021 article in Fortune Magazine, based on a study by business schools of Columbia University, Northwestern University, Stanford University, and the University of Southern California, found that in the Great Recession, mortgage delinquencies jumped from 2% to 8%. But in the pandemic’s first seven months they fell from 3% to 1.8%. “This is especially striking,” the researchers note, “given an unprecedented increase in the unemployment rate that reached almost 15% in the second quarter of 2020.” And, they found that the explanation went beyond just stimulus checks. Fast forward to 2023. TransUnion’s (NYSE: TRU) 2023 Consumer Credit Forecast projects delinquency rates for credit card and personal loans to rise to levels not seen since 2010. Card delinquency, on the rise in 2022, is projected to increase to 2.6% through the end of 2023, which would represent a 20.3% increase year-over-year. This is attributed to persistent inflation and high interest rates. Bloomberg predicts that credit-card rates are poised to hit a four-decade high this year. Bankrate predicts an average interest rate of 20.5% in 2023. And some retail-brand credit cards have already surpassed 30%. Just to give you an ideas, pre-pandemic credit card interest rates were around 17%, but fell below 16% when the pandemic hit. Which brings me to my point: the reason why credit card interest rates when down during the pandemic was to help people and help banks keep delinquencies low. Banks and credit card companies now need to heed what they did during the pandemic to avoid a repeat of the Great Recession. Here are six strategies financial institutions, including credit unions, deployed during the pandemic that should stay in effect now: 1. Utilize forbearance. Instead of cracking down on delinquent borrowers, offer forbearance. That way, borrowers can delay loan payments without you declaring the borrower delinquent. It also improves your borrower relations by not diminishing the borrower’s credit rating. You will still take a hit on revenue, but only temporarily, and you don’t have to worry about a portfolio of foreclosed assets to liquidate. 2. Offer a variety of payment options. You can decrease your delinquencies by offering various payment options to your borrowers. Anyone struggling financially can pay principal-only, interest-only, or a combined payment. You could also reduce the minimum payments if possible. Be creative. 3. Encourage recurring payments. Offering recurring payments makes bill payments easier and more timely. This is especially helpful for busy borrowers or those who travel. 4. Encourage paperless adoption. Studies show that those borrowers who receive electronic bills tend to be more satisfied and reliable borrowers. According to an article from My Billing Tree: “By encouraging paperless adoption, you are in turn developing a more satisfied customer base. These customers, in many cases, are then more likely to be receptive to other types of account management features, including enrollment in recurring payments.” 5. Accept payments regardless of method or channel. In addition to different payment amount and delivery options, you can also provide different payment methods and channels. Borrowers can call and pay by phone, or even text to pay. 6. Improved information from technology. With online and mobile banking, borrowers can check their balances in real-time. Upcoming loan due date reminders can be emailed or texted to them. Pending payments can be posted to avoid overdrafts. We cannot overestimate the importance of technology in avoiding delinquencies and making borrowers happier. Loan delinquency rates could improve more, due to robust employment numbers. The important thing to remember is that most borrowers want to pay their bills and pay them on time. With these proven methods, credit card companies and banks can do their part to help with the economic challenges their members have. By smartly learning from the past, financial institutions can improve their delinquencies, borrower satisfaction, and bottom line. A previous version of this article was published on CheckAlt.  Photo by Patricia Prudente @apsprudente … even if you are making a profit. Working Capital is the lifeblood for most businesses. It can make the difference between surviving and growing or going bankrupt. Working capital is all about planning, negotiating and timing. Oftentimes, owners learn this the hard way. After leaving the investment banking world, my then husband and I started our own business. According to family folklore, his father’s plastic manufacturing business had patented the original Hula Hoop which was featured on The Art Linkletter Show and immediately became a worldwide fad, its sales estimated to be over 100 million hoops in two years. After those two years, his family went back to their regular plastic extrusion business for OEM customers like automotive companies and the like. Whamo registered the name and continued selling them, albeit in much lower numbers. At the 50th anniversary of the launch of the original, a cousin asked us to make hoops for their chain of American Greetings stores which numbered about 50 or so. We updated the colors to fluorescent shades and they looked fantastic. We named the hoop the Maui Hoop and called our company Maui Toys. We invented three more products, went to our first trade show, the International Toy Fair in New York City, and our toy company was off and running. Maui Toys was soon selling to large retailers such as Toys “R” Us, Walmart, Target, Kmart, Children’s Palace, and a slew of other smaller chains and independent toy stores. It was great fun, but we were facing a looming working capital problem. We were self funded and it was one thing to make a few thousand hoops for one smallish store chain, and it was another to make hundreds of thousands of hoops for huge chains such as Walmart. Working CapitalBefore I get to our survival strategy, let me explain what working capital is for those who don’t know. It is the money a business needs to cover the gap between paying bills for its manufacturing or purchases of its products and collecting money from the sales of those products. This can pose a problem. Why? Let’s use the example of making hoops. You order your hoops from a plastic manufacturer, in this case a plastic extrusion company. Think of extrusion as the famous Play-Doh machine where you put a ball of doh in the little mechanism, a shape at the end (called a die) and you push the Play-Doh through. It comes out as a long tube of doh in whatever shape you have chosen. Obviously for the hoop a circle die was chosen. Your extruder makes your products and gives you a 30-day invoice which means you have to pay them in 30 days for the plastic tubes. Let’s assume that bill is $250,000. Then you have to pay factory workers for assembling the hoops in a circle with a connection plug, put a label on it, and pack it into a box for shipping and displaying at the store. Your toy company has to pay the factory workers their salary in addition to payroll taxes bi-weekly. You also have to buy a label from a printing company. It’s a small expense but has to be paid up front until you can establish a credit relationship with them to get 30-day terms. Let’s say all of that costs roughly $14,000. Most of it has to be paid in 30 days or less. You ship your boxes of hoops to your biggest customer and invoice them. They have 60 days to pay you and you find that they often stretch that out to 90 days and sometimes even 120 days. According to the following, hypothetical and very simplified cash flow/working capital projection, by month 4 you need almost $278,000! That’s assuming your customer pays you in 90 days and you have to pay your plastic manufacturer in 30 days.  Timing You’ve had to spend about $280,000. Your invoice to your customer is $500,000. There is a lag effect where you have to come up with almost $280,000 dollars to pay your suppliers and you won’t receive your $500,000 from your customer for another 90 days. That’s a working capital problem. By the way, you’ve just made a huge profit. But, how do you bridge the 60, 90 or 120 gap between paying your bills and receiving your money? Hard to put $280,000 on a credit card. Maui Toys didn’t have that kind of money. Nowadays, founders might raise money as seed capital from an investor and give away a percentage of their company’s stock. We came up with another solution. The number one reason why we were able to survive and grow our business: We asked our plastic manufacturer to accept 120 days for our company to pay their invoice. They said, yes. They gave us 120 days to pay our bills. Technically, they gave us 30 days and we didn’t pay for 120 days. And they didn’t sue us. Or shut us off from future purchases. Labor and other costs still had to be paid for, but they were a relatively small percentage of the overall cost so we were able to cover that ourselves. We were lucky because we didn’t have to give away ownership to get started. In the startup world that’s called bootstrapping it.  Increase Your Working Capital

To summarize, these are the steps you can take to increase your working capital.

And remember, the truth is always in the numbers. Originally published at https://www.datadriveninvestor.com on August 10, 2022.  What is McDonald’s business? Some might say, the fast food business, or more broadly, the restaurant business. But what many people don’t realize is that McDonald’s is really in the real estate business.

Their real estate holdings include land and prime building locations around the world where their Franchisees build restaurants and pay them rent, month-in and month-out. That’s where McDonald’s makes most of their money, more money than selling burgers. I remember watching, “The Founder,” a 2016 film about McDonald’s history. “You don’t build an empire off a 1.4% cut of a 15 cent hamburger, you build it by owning the land on which that burger is cooked.” Decent flick by the way if you haven’t seen it. Southwest Airlines flies people around, but they are also adept at buying and selling oil futures. They do it really, really well. What started out as a way to hedge against fluctuations in fuel prices back in 2007, ended up being a major profit center for them. And while other airlines were losing money when oil prices skyrocketed, Southwest made money. Another good example is Amazon. According to a February 2022 article in Investopedia, while the majority of Amazon’s revenues comes from online and offline retail sales, the majority of its operating income is from AWS or Amazon Web Services. It is the world’s most comprehensive and broadly adopted cloud platform. Many car companies earn very thin margins selling cars but make up the difference both through financing those cars and inside their service departments. So are they in the car selling or the car servicing/repair business? Are they in the financing business? Of course it depends on the particular car company. Which begs the question, do you know what business you are really in? The best way to find out what business you’re in is to give the different departments (or product lines) inside your company their own financial statements. That amounts to extra accounting work, but not that much compared to the benefits that knowledge will give you. Break down each department’s sales, cost of goods sold, and expenses specific to them. You can apportion the time expense of employees who manage and work for different departments. You can also apportion rent, utilities, equipment, and so on. Then analyze and compare the financials. Which department is making the highest profit margin? Which one is generating the most cash flow? Chances are, that’s your core business. Why is this important? This is important because once you figure out what your real business is, you have to protect that and feed it. Spend extra money to make sure it is well staffed and well stocked. Veer marketing and advertising dollars in that direction. Give it the most attention. Doing this will protect your overall business. When I was a partner in the apparel business, XLARGE Clothing, we had half a dozen retail stores in addition to selling to major retail chains, bougie boutiques, and international licensees. What business were we in? XLARGE designed an entire collection four times a year: spring, summer, fall/back-to-school and holiday. The collection included everything from graphic tees and sweatshirts to jeans and work pants to accessories (belts, backpacks, etc.), to button down shirts to outerwear and even shoes. We did a lot of collaborations too with artists and other designer brands like, Vans and The Hundreds. Our retail stores were in San Francisco, Orange County, SOHO, and Los Feliz. Licensed XLARGE stores were in London, Germany, Taiwan, China, Hong Kong, Australia, Korea and Japan. The licensed stores had to buy all their clothes from us. We had a girl’s line, X-Girl and later, x’e. And our kid’s line was called, X-Little. And we sold to retailers such as Urban Outfitters, Bloomingdales, Journeys, Hot Topic, Federated Department Stores, PacSun, and many other cool stores like, Colette in Paris. It was really the best job in the whole wide world. The Beastie Boys were partners and we had a lot of great parties and store openings. Many wonderful artists worked for us and with us. My duties included traveling to Tokyo and New York City. It was hard work but great fun. Work hard. Play hard. Where do you think we made the most money? Well, it certainly wasn’t our retail stores. Retail is a difficult place to make money even with the vertical integration and resultant hefty gross profit margins that affords. We didn’t make that much money for most of our clothing collection either. Our volume wasn’t quite high enough to get the pricing we needed to be competitive. Most of our licensees had one or a handful of stores so they didn’t really buy enough from us to be a contender for our largest generator of profits. Diversification is good and we had many different sales channels that helped us achieve that; we didn’t want to throw out the baby with the bath water so we carefully evaluated all our different departments. Our true business, our real business, the thing that made us the most money was two things: graphic t-shirts and sweatshirts, and our Japanese licensees because they had eighteen stores. Nothing else came even close. Since I was the CFO, I closed most of our stores except SOHO and Los Feliz and wrote off those losses as advertising expenses, because that’s what they were. We also quit selling to most of our wholesale accounts because they weren’t worth the expense of a sales force and the merchandise returns were shameful. There were more things we shuffled around and refocused on. We hired additional, talented graphic designers for more tees and sweatshirts. We transferred the manufacturing of the collection to our different licensees and they had to pay us simply a licensing royalty instead of buying the entire collection. They still had to buy tees and sweats from us. All of these moves made our company immensely more attractive to the point where we were able to sell it to our Japanese licensee for a spectacular return. XLARGE is still around today and still a super cool, niche, streetwear brand. All of this analysis taught us we were in the business of making t-shirts and sweatshirts and selling them to Japan. The role of the customer. Sometimes a less profitable part of your business feeds customers to the more profitable part of your business. It’s similar to a loss leader in a grocery store. Using the car dealer example above, perhaps they make most of their profits in car servicing, but without selling customers the cars in the first place, they wouldn’t have a servicing business. That needs to be taken into account as well and can be established by doing a customer analysis. Think of it like computer analytics which tally where your customers originate. Are they being referred from a blog? Your website? Google searches? Social media posts? You should be able to track that. If most of your customers are coming from outside your website, then don’t invest too much time and money on your website. Or if the bulk of your business is coming from social media, then don’t spend money on Google ads. The important thing is to know your business. Know where you make the most money, what has the most potential and where your customers originate. Then spend more time nurturing those things. And remember, the truth is always in the numbers. Originally published at https://www.datadriveninvestor.com on May 12, 2022.  Road Trip with Raj@roadtripwithraj Road Trip with Raj@roadtripwithraj In the next couple weeks, a friend’s business is going to shut down and close its doors. Their customers canceled all outstanding orders. The only channel left for them is online sales, where their gross profit margin is 4%. Yes, gross profit margin, not net profit margin. In the meantime, their overhead costs are continuing unabated, eating all their available cash like a Pac-Man at warp speed. How can this company be saved? I reflect on that now ghostly column started in 1952 in Ladies’ Home Journal, “Can This Marriage Be Saved”? A long time ago when I was a young girl, I would read my mom’s copy each month. Marveling at how poorly husbands and wives treated each other I thought, quite decidedly, that I would never ever get married. But if I did, I would never let my spouse treat me so shabbily! Even today, if you Google, ‘can this marriage be saved’, there are over eight million results ranging from deep psychological probing to reading the ‘signs’ to taking pop quizzes, ostensibly because you cannot read the signs. If you Google, ‘can this company be saved’, there are precious few results. Most are about saving money, a component to be sure, but not really about saving the entire company. The thing is, I’m not really interested in the question, can this company be saved? I’m more interested in how this company can be saved. I’ve had more than a dozen of my former clients and friends call me in the last couple of weeks. They are understandably concerned about whether or not their companies are going to survive. This is something on everyone’s mind in the age of Covid-19 and the lockdown of America and the rest of the world. It’s everyone from CEOs and investors to bookkeepers and shipping clerks. I suppose the good news is that we’re all in this together and to some extent, we can assuage ourselves with the camaraderie of the situation. But if you own or run a company, the most vital question is, can it be saved? And how can it be saved? Doug Yakola has been running recovery programs for over twenty years from the prestigious management consulting firm McKinsey & Company. In a post about leading a company out of crisis, he explains that even good managers are often working under a set of paradigms that no longer apply while letting the power of inertia carry them along. Nothing like a worldwide shutdown to shift your paradigm. The good news is, we all know that the rules have changed. So here we are, now what do we do? Leaders need to make tough decisions and act quickly. To navigate these challenging times, executive leaders need to make tough decisions, act quickly and remember that the number one goal is to save the company while minimizing collateral damage to your community and workers/employees. Every business is different to be sure, but these classic turnaround strategies will apply to almost all of them. I’ve outlined some steps to get you started, with additional detail below. Even if you don’t own a company, you can employ some of these strategies for your household.

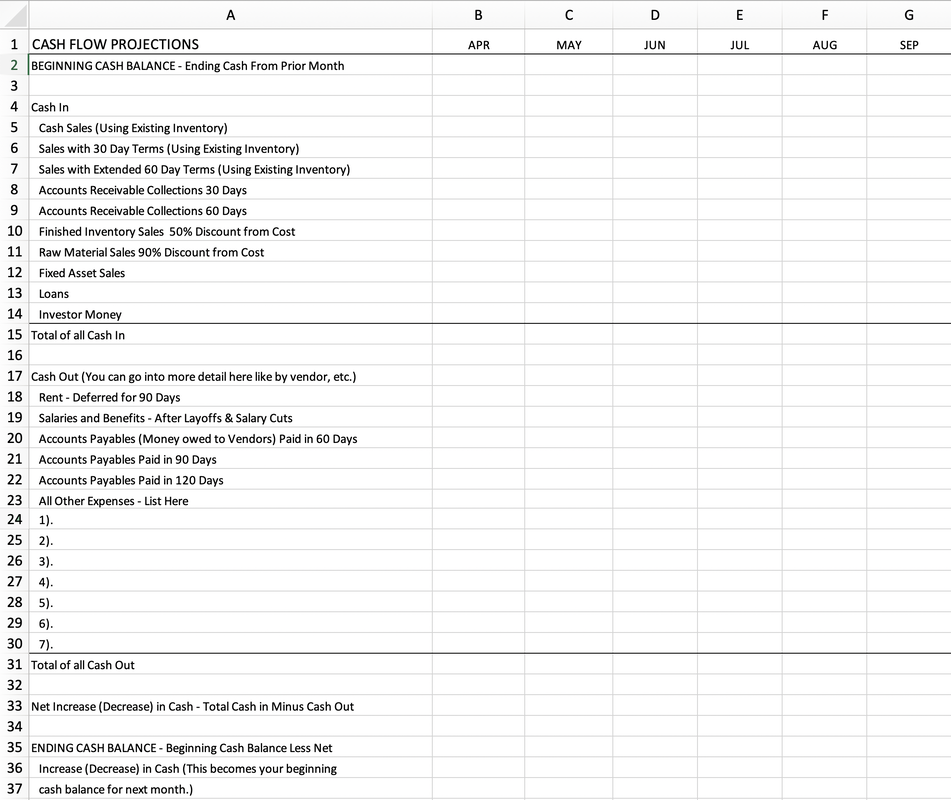

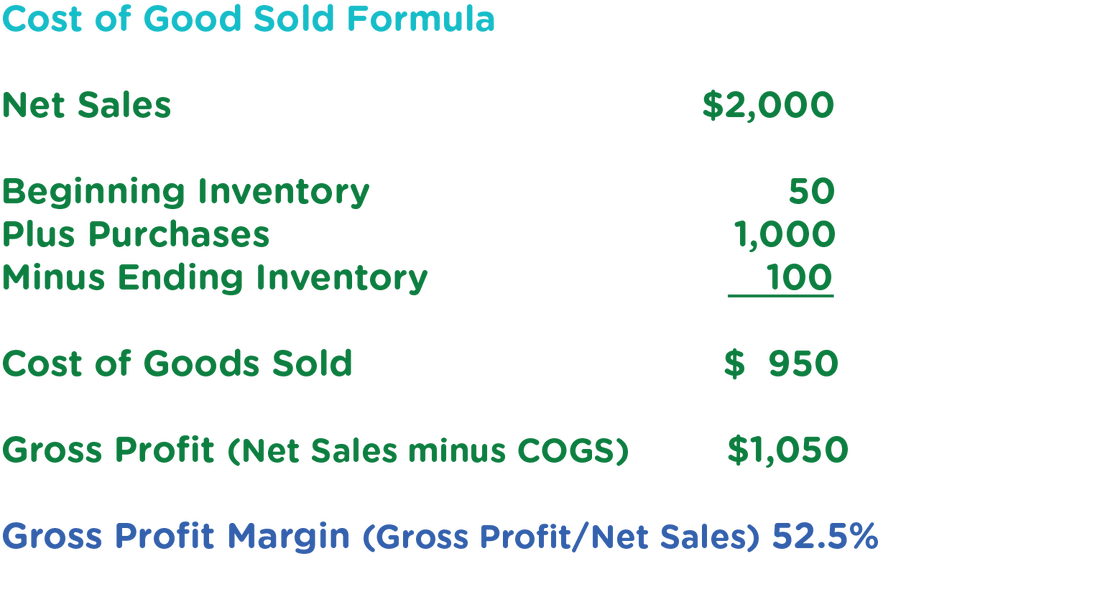

Don’t freeze. I know you may feel paralyzed right now, but the most important thing is to be in action — not motion, but action. What is the difference? James Clear explains it perfectly in his book, “Atomic Habits.” Motion is a planning process, a thinking, a mulling it over if you will. Action is actually doing it. Let’s say you want to write an article. Motion is sitting around thinking about it. Turning over the story in your mind’s eye. Maybe even doing research or making notes. But at a certain point, you have to sit down and write. That’s action. If you want to survive, you must be in action like Nike’s great slogan, “Just Do It”. Estimate how long this downturn will last. You may be wrong, but you may be right or only slightly wrong. Collect all the information you can and then take your best shot at estimating. That’s what projections are anyway — your most educated guess as to what is going to happen. If you at least have a set of assumptions and the resulting actions based on those assumptions, it is easier to make adjustments than it is to start from scratch or to have no plan whatsoever. Collect and hoard cash. See how much cash you have. This includes checking and savings accounts, bank lines of credit, credit cards, cash on hand, and investor commitments. (Confirm those commitments.) Tally up your accounts or loans receivable (money your customers or others owe your company) if you have any. Make an aggressive effort to collect all of that as soon as possible, even offering a discount if you can get a large portion now. If you have open lines of credit, borrow the maximum on them and tuck it away. Remember, in times of difficulty, Cash is King. Ironically, I recently wrote about that. You can find it here. As an example, last week when a large tenant of mine asked for a 50% discount on his monthly rent, I offered, if he paid me in full for April, I’ll waive the following two months rent. That would result in a 66% discount for him. But I’m getting the cash up front. Who knows? He may go out of business next month. His company perhaps cannot be saved. Salvage outstanding orders. How many orders can you save using existing inventory? Don’t make any new inventory unless you have an order that will use all of it and at a good price. Call all your customers. Maybe give them extra terms. Let them know that if they take your goods in today, you will give them sixty or even ninety days to pay for them. If they buy now, you’ll give them a discount. Better to get something for your inventory than to have it sitting in the warehouse. Project cash coming in. On a spreadsheet or piece of paper, write out the name of each month until you assume this will end. If you think it will be over in six months, then make the heading on top for the next six months — APR, MAY, JUN, JUL, AUG, SEPT, OCT. Write down your best estimate (based on the data collection you just did by questioning your customers), of your cash in — not just your sales — but when you will collect the money. Also include in cash, the amount of receivables you think you will collect under the month that you think you will collect them. This is the first part of a cash flow statement — when the cash is coming in. And be super honest and realistic with yourself. I’ve constructed a rudimentary Cash Flow Projection you can use as a template below. Project cash going out. If you are to make no changes, what are your expenses in the month the cash is going out? Look at keeping all your staff, paying your rent in full, payroll taxes, utilities, commissions, shipping, postage, etc. Subtract your monthly expenses from your estimated revenue. See what your shortfall is each month. If you have a shortfall of $10,000 every month and you have access to $30,000 in cash, then you’ve got three months of runway. That’s your worst case scenario. Now for the important part — let’s improve upon that. What are the two main categories of improvement? Increase or speed up cash in. Or decrease or slow cash out. Explore alternative sources for cash. As an example, find out how much money you can get from the SBA (Small Business Administration). The SBA is guaranteeing loans for companies and if you can keep your employees, it turns into a grant (which means you don’t have to pay it back). Make that adjustment of cash in the column of whatever month you can safely assume you’ll receive it. Can you liquidate any of your inventory? If you don’t have enough sales to use up your existing inventory (goods on hand or in your warehouse), then see if you can sell them for a “closeout” price — which usually means for ten cents to fifty cents on the dollar. If you are making a gadget that costs you $1.00, you will sell it for 50 cents. There are closeout companies in your industry. I guarantee it. Google it. Ask friendly competitors.They are out there. You’ll book a loss, but we’re concerned with cash here, not losses. Cut or slow down cash out. If you can slow down your payables (people you owe money to), or negotiate longer terms, or a lesser interest rate to your bank if you owe money, or deferred rent, or reduced shipping costs or wherever you can save money — do it and don’t wait. Like my friend, if all your sales are now online, then look at your server costs (believe it or not there can be a huge difference), drill down on your shipping costs, (pit Fedex against UPS or USPS), that’s a simple one and can be easily delegated. How can you save money on packaging? Boxes? Labels? If it’s a food company, it may be less expensive to overnight your items than pay for dry ice. Just be creative. Think outside the shipping box. Weed out lower profit margin products or services. Look at your product mix. You should know how much gross profit you are making on each product/product line. Gross profit is the sales price of a product or service less what it costs to produce or provide it. If it’s less than 30% of sales, consider dropping it. As an example, if your main product is pizza, but you supplement that by salads and wings and you make a 30% gross profit margin on wings, and only 20% on salads, then consider dropping salads from your line. It pains me to say this because I’m a vegetarian, but I’m not really your customer, am I? Trust me, there are still plenty of people that buy pizzas. If you don’t know your profit margins for each of your products, hire a good bookkeeper. I can recommend one. Or ask your accountant to help you (for a deferred payment or perhaps even barter). Free pizzas for life! Pun intended. Yes, don’t lose your sense of humor, not now as you may need some levity to balance the balance sheet of stress. Employees you should keep. If you are a consumer products company that sells to other retail stores, then your salespeople are gold. If you sell online, then your marketing people are gold. Look at where your business is right now, and lay off employees that you don’t directly need for what you’re doing right now. When things get back to somewhat normal, then you can re-adjust your employee mix. A word: please try to make this your last possible option. We’re all in this together and laying off employees will have ripple effects. If you can, perhaps try to pay everyone at half salary. After you’ve examined all of this — and this is not a gut instinct situation, this is an information gathering and numbers crunching situation, make a plan and meet with your stakeholders. They may include, board of directors, investors, and partners. Come armed with your six month projections and assumptions. Be forthcoming. If you have completely honest and well-thought out information and research backing up a Master Plan, they will be much more likely to support you. Schedule a meeting with your bank. If you need them to lend you more money, and show them your realistic and conservative Master Plan, you have a better shot. If you can’t make your payments on a timely basis, then tell them. As a former banker I can tell you one important fact: bank’s don’t like surprises. Yes, it’s true. Your bank or investor or factor will be much more likely to support you if you meet with them, clutching your Master Plan in hand with an up-to-the-moment financial picture. This is not an online dating profile with a ten-year old photo. They don’t want you to bullshit them; they not only want you to succeed, they need you to succeed. They don’t want to be left in the dark either. Give them the honest information up front and keep them updated with excruciating frequency. Weekly at minimum, daily if necessary. You would rather that they’re sick of you — “OMG, it’s her again” — than for them to be wondering, “what ever happened to her? I haven’t heard from her in months!” It’s probably not comfortable, but it’s always better. I have three final words for you: plan, plan plan. You must start and finish with a plan. Be conservative (provide a cushion). Change it as you go. Communicate it to everyone relevant. And remember, this too shall pass. Here is that Cash Flow Template I mentioned:   Many companies don’t really understand what a cost of goods sold is and don’t calculate it correctly. I’m going to tell you why that’s dangerous. I get endless writing fodder from my clients. I am currently working with a company that is acquiring another company. My partner and I were retained to calculate a valuation and propose an appropriate deal structure. Easy peasy. Right? Wrong. The target company is a manufacturing company and their cost of goods sold (COGS) was wrong in six ways from Sunday leading to an inaccurate gross profit margins. It is difficult to value a company without a solid COGS and gross profit number. Further, it is difficult to make decisions about your company if you don’t know what your COGS is.  COGS Formula Let’s start with the formula for COGS: beginning inventory plus purchases minus ending inventory. That’s it and it is logical. It’s what you started with (beginning Inventory) plus what you purchased to add to that (purchases) less what you have left over (ending inventory). Why subtract ending inventory? Logically, because it is the Cost of Goods Sold. If you don’t sell it, subtract it out and it will be your ending inventory for this period and your beginning inventory for the next period. Yes, it is calculated for a particular time period. For small companies that is usually monthly, quarterly and then at year end. The idea is that you want to find out exactly what it has cost you to make or buy the products you sell for that time period. So it is only that. Not sales commissions or whatever it cost you to sell them. Not what it cost you to store everything in your parent’s garage. Not what it cost you to make samples or go to trade shows or advertise. None of that. Just, what it costs to make your products. The only exception to this rule is if you are doing your own actual manufacturing. Then you can include factory overhead expense into COGS for the time period in question. Inventory Valuation To drill down to the component parts, inventory is the entire cost of your products to get it to your warehouse and only that cost. Not what you’re going to charge your customers or retailers. That’s your wholesale price (if your selling to stores) or your customer price (if you’re selling directly to customers). And inventory should always be the lower of cost or market value. So if it cost you $10 to make a widget and you make 100 widgets, then the total value of your inventory is $1,000. If the market value (what you are going to sell it for) is $5,000, your inventory number is still $1,000. ( Lower of cost or market.) But if the market crashes for your widgets and you can only sell them for $500, then your inventory should be listed at its market value of $500. ( Lower of cost or market.) A note about the gray area of inventory valuation It is very easy to manipulate your inventory to make more money or lose more money. It is the easiest way to affect profits and losses in business. Why would one want to do that? If you have bank loans that require you to make a certain amount of profit, you would want to value your inventory as high as you can. If you have a privately held company and your goal is to pay the least amount of taxes, you would want to write-off inventory that has aged, as much as reasonably possibly. I am not suggesting you do that because you need to show an accurate inventory valuation and you don’t want to get in trouble with banks or the IRS, however, it is something that is often done. Don’t do it. And by the way, it will eventually catch up to you down the road. Purchases Purchases should include the total that you paid for your widgets, $1,000 in my example, and how much it cost you to ship it into your warehouse or parent’s garage (part of your cost and called “freight-in”). If you are importing, you should also add in customs and duties as a part of the freight-in cost. Manufacturing  If you are manufacturing it gets a bit more complicated. In that case you have to add together purchases of all the raw materials required to make your widgets and still include freight-in that will hopefully be less than shipping it from a foreign country if you’re using parts made nearby. In this case your inventory number should also include raw materials and work-in-process (or progress), or WIP.

Let’s say you are manufacturing coats. You have an order for 80 coats at $25 each. Luckily you start out with 80 coats that cost you $12.50 to make. But you want to make more inventory in case you receive more orders. You buy the fabric locally and ship it to your factory. You also purchase thread, buttons, zippers and tags (raw materials). At the end of your reporting period, 12/31/22 (called a fiscal year), you had personal problems and were only able to cut the coats out of the fabric. Since you haven’t sewn and finished them, they are considered WIP. Your purchases would be all the raw materials that your company purchased along with the cost to ship them to you. Your ending inventory number would include any finished inventory (that you don’t have in this example), all of the raw materials that you haven’t used yet and WIP (which now includes all your fabric because you cut it). Your only sales (since you haven’t finished making your coats), were from beginning inventory or the coats you made from last period. Why your COGS is so very important Now that we know how to calculate an accurate COGS, let’s discuss why it is so very important. You need an accurate COGS to calculate your gross profit. You must have an accurate gross profit to make important decisions about your company, to price your goods and to ascertain if you’re making any mistakes so you can fix them. As an example, If your gross profit is too high, you may be charging too much for your products and by lowering your prices, you could increase your sales enough to more than compensate for your lower prices. If your gross profit is too low, maybe you are not charging enough and could raise your prices, sell the same amount and make more money. A major problem with a COGS that is too high, is that you purchased too much inventory. That eats into your COGS percentage as well as your cash flow. It can also be that you paid more than you estimated for your products or raw materials. Sometimes, freight-in costs can be increased at the last minute (a problem with many companies in the last year). I’ve even seen companies that forgot to add in an important raw material when pricing their product. Try to add a cushion into your pricing too account for problems that crop up. For more information about pricing read my November 2019 article, “The Art of Pricing.” Cash flow problems with inventory At a minimum, you must make enough gross profit to pay your overhead expenses such as design, marketing, sales, rent and salaries. If you purchase too many products, much more than you have orders for or more than you can sell, that is going tie up your money in inventory and you may not have enough cash flow to operate your business. I’ve seen many small companies go under because the cash they need to run their company is sitting in their warehouse in the form of inventory that can’t be sold. Often this happens because there are certain minimum order quantities they must purchase. And people think their products are great which they may be, but they are overconfident that they can sell them. For more information on cash flow, read my March 2020 article, “Why Cash is King and How to Get More of It.” In closing, keep a handle on what it takes to manufacture or purchase your products. It will be the foundation of your decision-making and most importantly, the source of your cash.  Photo by Andy Kelly on Unsplash Research suggests that up to 70% of partnerships fail to deliver their intended outcomes. That’s an incredibly high number and one that borders on emergency status.

I’m reading “Klara and the Sun,” by Kazuo Ishiguro. It’s a wonderful book about an A.F. (artificial friend) named Klara. Klara is delightful, curious and observant — a good A.F. And the story, told in a first person narrative with Klara being the narrator, adds an element of fascination. I find myself considering, wow, this is how a robot might “think”. Klara’s “life”, so far (I’m about halfway through), is relatively simplistic as you can imagine a robot’s life would be. She knows her place, is well-mannered, puts her real-life friend, Josie, first, and isn’t emotional about any of it. It got me to thinking about business, specifically partnership problems in business that often arise because partners don’t respect each other or are simply too emotional about their issues. I have one consulting client right now going through partnership challenges. They’re looking to sell their company to ostensibly buy out a couple of their partners. I also recently spoke to a potential client who is considering drastic steps with her company due to problems with one of her partners. And there’s more! Partnership problems seem to be coming to me more frequently of late. Sometimes I feel like I should have a degree in psychology instead of economics. It brings to mind my own relationship with my partner in my last company. We worked together for twenty four years, sold our manufacturing company after my twelfth year, bought commercial property and multi-family housing units and kept going together for another twelve years investing in real estate. We did very well. In all our years working together I can’t remember one significant fight or argument. After much thought, I put together a list as to how I think we accomplished this.

None of these things is revolutionary. Everyone can do them. Treat your partner like you would like to be treated. Even minority partners. If they want more information, give it to them. If they want annual meeting notes, write them. Have mutual respect and keep your emotions in check. Remember, it’s not personal. It’s business. In short, be more like Klara.  Photo by Aaron Burden on Unsplash Business is stressful because things are always going wrong. As a CEO you might wonder, when is this going to end? When will it get easier? What level of sales or profits do I need to attain? At what point will my business be strong enough and healthy enough that I’m not constantly worried it will somehow crash and burn? I was a founding member of a group of entrepreneurs called, The Startup Founders. We were all in various stages of starting and growing businesses. As we grappled with the day-to-day challenges that a startup must shoulder and solve, the group gave us a safe place to process “issues.” They could be anything from problems with a partner or in my case, a substitute for not having a partner. There were also the questions relating to raising money, formulating a business model, or pivoting when that model wasn’t working. It was a case of helpful collective intelligence. One day I was talking on the phone to a fellow member who came up with a brilliant idea relating to photo storage. She was complaining how difficult the process was, and how she was so tired of fighting through all the problems that kept appearing at her doorstep, like that trick-or-treating kid who kept coming back for more candy. At one point she cried out, “When is this going to get easier!?” Before I answered her, I thought of a great book I had read that perfectly answered this question. It’s actually one of my top ten business books, “Losing My Virginity,” by Richard Branson, and I highly recommend you read it. The subtitle is, “How I’ve Survived, Had Fun, and Made a Fortune Doing Business My Way.” A little wordy to be sure, but it well describes the contents and pearls of wisdom contained therein.  Reading about Branson’s trials and travails when he started Virgin Airways is when I had my epiphany: It’s always hard and it never gets easier until you sell the company.True story. Even when Branson was running an actual airline and he was a billionaire on paper, he was still fighting with British Airways almost every single day in addition to all kinds of problems like labor and mechanical issues and scheduling and cash flow and raising money and paying off debt and … you get the point. As Roseanne Roseannadanna, played so brilliantly by the late Gilda Radner used to say, “It just goes to show you. It’s always something. If it’s not one thing, it’s another.” And that was my epiphany. It’s always hard and it never gets easier until you sell the company. If it is hard for Richard Branson, it sure as heck isn’t going to be any easier for me, for us. I told my friend that. I told her that it’s never going to be easier until she sells her company and just knowing that, going into it, makes it easier. Right? If you know this, you can roll with the punches, you can not be disappointed when your expectations are not being met, because basically, you cannot have any expectations. You just take it one step, one day at a time. And then you’ll be fine! Trust me! I’ve built three companies from the ground up.  It also brings to mind another one of my top ten business books, “How to Stop Worrying and Start Living,” by Dale Carnegie. It is chock full of helpful methods and processes to actually cure your stress and worry problems. Chapter 3 in his book is called, “What Worry May Do to You.” In that chapter he quotes Dr. Alexis Carrel, Nobel prize winner in medicine: “Businessmen (okay, it was written in the 40s) who do not know how to fight worry die young.” Then Dale Carnegie gives you multiple ways and means that you can deal with your stress and worries. I’ve read this book dozens of times.

In an earlier Medium Article I talk about one of his methods that has worked for me every time, “Before You Freak Out, Ask Yourself These Four Questions.” In the end, my friend didn’t move forward with her business. The biggest issue was that Google happened to come out with a product very similar to hers and she felt that it didn’t make sense to continue. Understandable. At least she knew early before she pumped more money into her venture. I’ve shared my epiphany with many others since that time, with the hopes that it would help them manage their expectations. I believe that it has helped. I know that it has helped me. P.S. Congrats to Sara Blakely for selling her Spanx business to Blackstone yesterday. She can now take a well-deserved, deep relaxing moment. I’m sure she’ll be back at it soon.  Photo Credit: Ashton Mullins on Unsplash and how to get more of it.

In the last two weeks, my stock portfolio dropped significantly in value, and I don’t care. Why? Most of my stocks are dividend paying and thus far at least, the dividends haven’t been cut. What matters is the cash they’re generating which I depend on for a part of my income. That hasn’t changed. Also, I’m quite a ways from retirement, so I can sit tight and wait for the next upswing. The cash generated through dividends is more important than the value of the underlying stock. Cash is king. You may have heard that old saying. Basically it means that cash is more important than the value of assets or even your profits. And most of the time it is. Here’s another example. I bought a house with a 30-year fixed mortgage. My mortgage payments were not going to increase. I worked my monthly payment into my budget, and I knew, based on my income, that it was affordable as long as my income didn’t decrease — not likely. Then, the Great Recession of ’08 happened. My house dropped significantly in value and I didn’t care. Why? My monthly payment remained the same, my income remained the same, and I wasn’t going to sell my home anytime soon if ever. The value of my house didn’t matter and I knew it would go up again eventually because it is in a great neighborhood. And it did. Cash for Your Business What is a cash flow statement? It’s cash in less cash out. If your business is cash flow positive every month (more money is coming in than going out), you’ll be okay. What is an income statement? It is revenue or sales, less expenses. The result is your monthly profit or loss. You can operate at a loss for a period of time, and as long as you are cash flow positive, you can still be okay. Here are some suggestions for how to manage your cash flow in a business:

Cash for Your Personal Life As far as your personal life, there are several ways you can make sure you have adequate cash on hand for emergencies. Here are some tips:

The bottom line is that you want to always have cash on hand one way or the other for both yourself and your business. Cash is king.  Photo by life is fantastic on Unsplash I invented one of the coolest new products in my industry (gardening) in the last fifty years and I didn’t know how much to charge for it. I knew after all my years in business that the one thing that probably has the biggest effect on sales is pricing. And most people have no clue how to set a price which can be equal parts, psychology, research, analytics, and trial and error. An enterprising attorney I had met some time ago at the Licensing Expo in Las Vegas, set up a meeting with Vince Offer — the ShamWow pitchman legend who had become somewhat of a cult star with the millennials. He was interested in featuring my newly released product, the VeggiePOPS seed starters (now called SeedPops), on one of his infomercials. We met in nearby Santa Monica for coffee where he divulged that his name was really Offer Shlomi, and that he changed his name to Vince because he was a huge fan of Vinnie Barbarino, John Travolta’s character on the iconic 70’s television show, Welcome Back Kotter. “What a coincidence!” I said, “Because my ex is the late Robert Hegyes who played Juan Epstein in Welcome Back Kotter, and they were close friends.” John is the Godfather to Bobby’s daughter Cassie, who I raised as my own (and helped me develop the SeedPops). Vince was a fascinating guy who innately knew more about pricing than just about anyone I had met in my thirty years of business. Vince went on to explain that before he agreed to take on any particular product, he insisted that a booth be set up at the Rose Bowl Flea Market in Pasadena so he could see first-hand how well the product sold. I had previously been a cofounder/partner in two successful companies — toys and apparel — and we sold to mass merchants like Target and Walmart for the former and “high-end” department stores like Bloomingdales and even Barneys for the latter. The idea of selling at a flea market seemed beneath my pay grade, but I agreed to his terms with curiosity, and wow, (or Sham-Wow), I was glad that I did. I secured a booth at the flea market and roped Bobby’s son, Mack, who I also helped raise, into helping me transport, set up and man a pop-up tent, boxes of product, folding table, etc. and we embarked at sunrise for the Rose Bowl on a sweltering August morning, the second Sunday of the month. After setting up, we stood behind the table as buyers strolled by. I displayed the Pops on several lollipop stands — each holding forty eight. The whole presentation looked immensely colorful and appealing. Initially, when attendance was sparse, people would stop, marvel at the Pops, and buy one or two. We had priced them at $3.99 each. By lunchtime we had sold about half a single display — 24 pops. How did I come up with that price? I used Cost Plus pricing, defined more fully below. In addition, I researched packets of non-GMO, organic seeds and found that they ranged from about $2.00 to $4.99 depending on the vegetable, seed packager and store. My price point of $3.99 seemed reasonable. Around lunchtime, Vince Offer showed up, looked around the table, observed the people buying the Pops, and after awhile said, “This is what we’re going to do. You have six different colors, six different vegetables. You’re going to offer people (Offer, ha!), $20.00 to buy five and we’ll give you the sixth Pop for fee.” Within an hour, we had sold out. In terms of price, that amounted to $3.33 per Pop instead of $3.99. Price Setting Checklist Does the World Need Your Product? This is a tough question and not really within the scope of this article. There have been entire books written about it. I recommend reading, The Lean Startup, by Eric Ries. A good place to start by asking, “Is this a product that I want or need or could use that I can’t find in the marketplace?” To quote an old saying, “Can I build a better mousetrap?” Or, “Can I make the mousetrap more affordable? Prettier?” I recommend starting by observing your closest competition. Competitive Analysis If you are making a product that is not patented or otherwise protected, and other companies are making a similar product for $50, you are not going to be able to charge $100.00. So, keep that in mind. If you cannot do it for $50 without losing money, then you’re probably in the wrong business or you have to closely examine your costs and see where you can save money. Also, if you can somehow give the impression that your product is super special, build your brand awareness so that everyone wants your baby doll or cashmere sweater, then you can charge more. Building brand awareness is hard and expensive though. If you are making your shirt out of silk and your competitor is making it out of polyester, you can charge more for yours. If your workmanship is superior, you can charge more for that. And it depends where you’re selling it, too — online stores or brick and mortar. These are all considerations in setting a price. So start with a competitive analysis. List all your direct competitors and what they are charging. Make a note of how they have differentiated their products. For me, I knew that there are a lot of seed starters out there, but they are all the same, all brown and boring cups, and I felt like I could build a better mousetrap. Also, I had been working with schools putting in school gardens for several years. I noticed that there are three things that made a big difference:

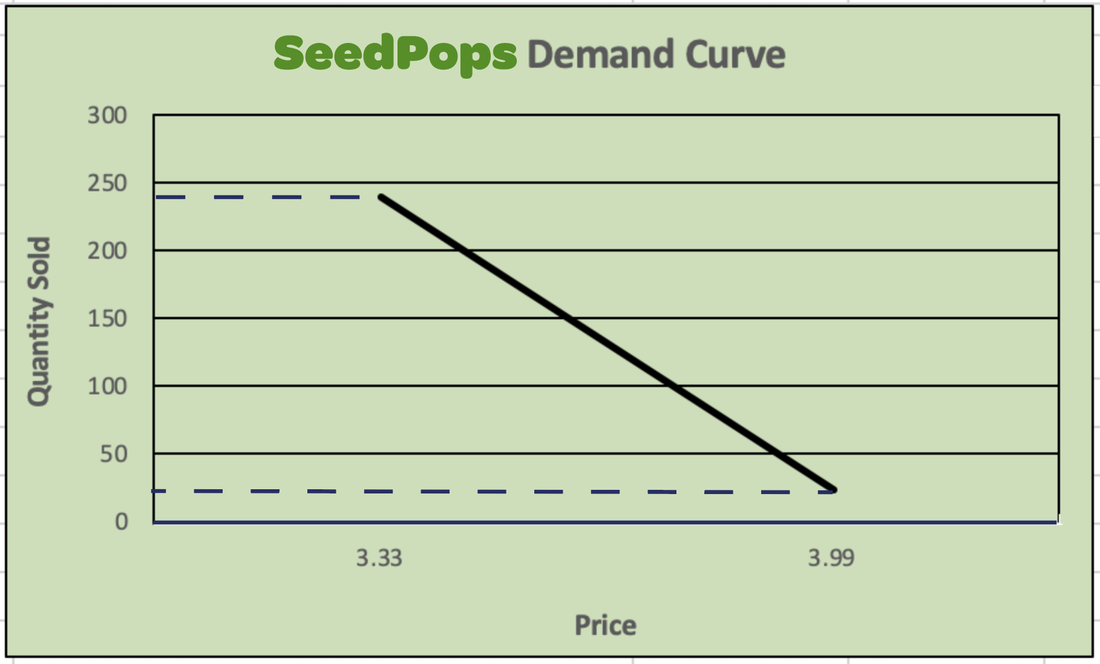

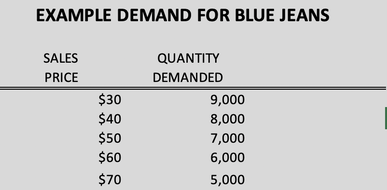

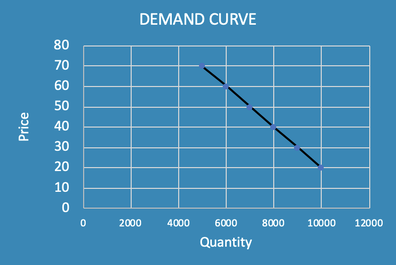

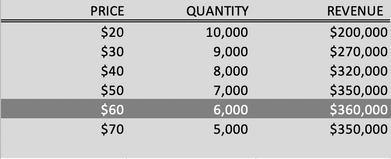

I knew I could build a better mousetrap and together with my daughter, Cassie, we set about building a better mousetrap — hence, the SeedPops were born or created as it were in our kitchen with newspaper, my food processor, some donut hole trays, paint, soil, fertilizer, seeds, and my oven. But what would we charge for them? A lot of pricing decisions come down to competition, but, there are also pricing models to consider and they all have their plusses and minuses. Choose a Pricing Model Pricing of course, depends on what you are doing, e.g. software, consumer products, business to business, services. There are a lot of different pricing models and you’re probably personally familiar with most of them. Believe it or not, one pricing model is “free”. You may recognize Facebook or Twitter as free pricing that later — when they had enough users –could charge for advertising. There is also: subscription, freemium, hourly rates (many service providers), project-based, value-based pricing, equity pricing, velocity pricing, and cost plus pricing to name some. You can look all of these up, but for the purposes of this article, I’m going to focus on cost plus because that is where most of my experience lies and that is the most common method for consumer products. And I’m going to focus on selling directly to the consumer such as an online store or in my case, the flea market. It is the easiest way to go into business because you are not dependent on selling to a store and you can easily try different prices. Cost Plus Pricing Defined I have a friend who is a new entrepreneur and recently started her own apparel company with a really cool product. I’m a hard sell and I love it. She is concerned that her online price matches her store price and are her prices too high? Are they too low? Is she making enough money to make her side hustle worth it? What should her sales channels be and how much should she charge for each of them? Should she put her products on sale? And when? I explained to her the idea of the cost plus pricing model and told her to start with that. Cost plus starts with a very accurate cost sheet including every tiny thing — every label, thread, tag, fabric, pattern, cutting, sewing, and so on. After adding all of your costs, double them — and that becomes your wholesale price. If you sell to a brick and mortar store, they would typically double it again for the end consumer. Understand that doubling the price is a 100% markup. The Importance of Accurate and Complete Cost Sheets What you don’t want to do is make a careless mistake on calculating your costs that will affect your sales price. I’ve seen that happen. You cost your sewing at $5.00 an item when it’s really going to be $15.00. How do you determine your costs? Get firm quotes in writing from all your subcontractors and suppliers. When I say you have to include every teeny tiny item, I mean it. Not just printing your hang tag, but the cost of the safety pin that attaches the tag. The plastic bag that you place your item in. Everything little thing. Make a spreadsheet or list it out on a piece of paper, it doesn’t matter what method you use. Just make sure you are accurate. This is vital because you don’t want to price your product below your cost. Sounds obvious, but if your costs are inaccurate, how do you really know? Minimum Order Quantities or MOQs If you are buying component parts from another manufacturer and most likely you will be, make sure you find out if there are minimums (MOQs) that you have to buy. Example: You are in the apparel business. You are going to print your fabulous graphic designs on camouflage t-shirts and sell them. You think you can sell 500 shirts to your friends. You go to your t-shirt manufacturer and put in an order for 500 camouflage t-shirts. She says, sorry, our minimum is 1,000. Don’t do it. Haggle with her. Or, find a manufacturer who will sell you 500, even if you have to pay a premium. A very wise person (my accountant) taught me a saying for manufacturing or assembly: First Loss is Best Loss. In other words, better to write-off fabric at $10.00 a yard than completed garments which use that fabric, plus sewing cost, thread, labels, etc. Fabric is a smaller loss than a finished garment. The most common reason why companies go out of business is because they make too many products (inventory) and all their money is tied up in those products that they can’t sell. Because we are using a cost plus pricing model, the direct to consumer sales price has to be at least double your cost — more if you plan on selling to brick and mortar stores later because they will have to take their 100% markup. For my example, because I was selling directly to the consumer, e.g. the Rose Bowl Flea Market, or if you selling through your own online store, you have the ability to do an A B Testing of sorts. You can change your price and see how that affects your sales! That was the genius of Vince Offer. Construct Your Own Demand Curve A typical Demand Curve is negative. This is just common sense. The more you charge, the less you sell; price and quantity have an inverse relationship. This is a microeconomic concept and like anything in economics, it’s sometimes more of an art than a science. Why? Because other things may come into play — like the time of day or the weather or one location is better than another. That’s why it’s good to try to hold all other things equal. This is obviously difficult if you are selling to brick and mortar retail stores because you sell to them in bulk and they set their own price. You can’t sell them two sweaters at $20.00 and 5 at $30.00. But if you are selling online directly to the end consumer, you can easily change the prices. That’s why I recommend you launch your product first by selling directly to the consumer. Here is the very simple Demand Curve from that day at the flea market.  Pricing Psychology You can see that when I charged $3.99, I only sold 24. But on the same day, with the same product, in the same place, when I lowered the price to $3.33, I sold 240. I didn’t sell it like that though — putting the price tag at $3.33 — I sold it in a different way: buy five get the sixth one for free. That is where the psychology comes in. People liked that they were getting all the different colors and all the different vegetables and they felt like they were getting it for a deal. Which they were. Another way that psychology comes into play is when will buy more if the price is higher. This is called a Luxury Demand Curve — people think they are getting a more valuable item if the price is higher so they buy more. What Price Generates the Highest Sales? After you test your different price levels, you should then figure out which price generates the highest sales volume. Your total sales or gross sales are just the quantity sold multiplied by the price. In my SeedPops example, clearly, my total sales were much higher at $3.33 vs. $3.99: $799.20 vs. $95.76 respectively.  But let’s say you are selling blue jeans and the sales numbers were closer at the different prices. Your customer’s demand might look like this chart to the left.  And your Demand Curve would look like this chart. At $30.00 you are going to sell 9,000 pieces and so on. But what price will give you the optimum sales (also called revenue)?  Let’s calculate what your sales are at these different prices. Here we see that the highest revenue made is from pricing the jeans at $60.00. Emotional Considerations

Almost worse than inaccurate costing or building too much inventory is to lowball your price because maybe you have an inferiority complex or you don’t think your products are worth it or you don’t think you are worthy or deserving. You’d be surprised how often this happens (including with yours truly). Remember these four rules:

If Vince had told me to sell my SeedPops at $1.50, I wouldn’t have done it. Recap on Pricing

Final Note: you don’t have to make excuses for your pricing and I don’t think you really have to apologize for early adopters that your prices are now lower. Think about the first customers for the calculator. They paid hundreds of dollars for something that we get for free on our phones. Hewlett Packard is not worrying over the fact that early customers paid $200.00 for one of their calculators. And what happened to me and my SeedPops? I decided not to do an infomercial with Vince — I went the way of getting a licensee to license my invention. They do the manufacturing and sales and pay me a royalty. My SeedPops are now found in thousands of stores all across North America including Target. On a side note, my attorney also asked a friend of hers to meet me at the flea market that day because he was a consultant that helps companies expand overseas. I am currently in talks with a Dutch company to sell SeedPops in Europe, and a company for Australian distribution. That consultant and me? We are now a couple. Happy ending. I’d love to hear your experience with pricing and any questions you might have. |

Stories and snippets of wisdom from Cynthia Wylie and Dennis Kamoen. Your comments are appreciated.

Archives

February 2024

Categories |

The Project Consultant

Post Office Box 469

Venice CA 90294 USA

Post Office Box 469

Venice CA 90294 USA

© 2024 The Project Consultant. All Rights Reserved.